In the realm of tax compliance, mistakes are often made—whether due to ignorance, oversight, or sheer error. However, the Income Tax Act of India offers a second chance to taxpayers through a provision known as the Compounding of Offences. It is an opportunity to rectify violations without facing the harsh consequences of prosecution, fines, or imprisonment.

But what exactly does “compounding of offences” mean under the Income Tax Act, and how can it work in your favor?

In this article, we’ll explore the concept of compounding of offences under the Income Tax Act, its benefits, and why it’s a valuable option for taxpayers who find themselves on the wrong side of the law.

What is Compounding of Offences?

The concept of compounding of offences refers to the process whereby a taxpayer who has committed a tax-related offence can settle the matter with the tax authorities by paying a specified amount as a penalty, without going through the criminal justice system.

Think of it, to clear up issues without going to court — faster, easier, and less stressful.

Compounding of Offences, it is governed by the following Section of the Income Tax Act, 1961:

Section 279(2):

This section provides the authority for compounding offences. It states that any offence under the Income Tax Act may be compounded by the Principal Chief Commissioner or the Chief Commissioner of Income Tax, either before or after the institution of prosecution.

Which Offences Can Be Compounded?

Not every violation can be compounded. Under the Income Tax Act, compounding is available for specific types of offences, such as:

- ✦ Failure to furnish returns or concealment of income.

- ✦ Failure to comply with the assessment or to attend proceedings.

- ✦ Failure to deposit tax deducted at source (TDS) or tax collected at source (TCS).

- ✦ Failure to produce accounts and documents as required under the Act.

It’s important to note that serious offences, such as those involving fraudulent evasion of tax or substantial financial misdeeds, may not be eligible for compounding. The decision to compound is ultimately at the discretion of the tax authorities.

The Process of Compounding Offences Under the Income Tax Act, 1961

Step-by-Step Guide to Compounding:

Here’s how the compounding process works:

Application Submission: You need to file an application with the Principal Chief Commissioner or Commissioner of Income Tax.

Eligibility Check: The authorities will check if the offence is compoundable and whether you meet all the conditions.

Fee Payment: Once approved, a compounding fee is calculated based on the nature of the offence and other factors. After payment, the case is closed.

Issuance of a Compounding Order: Once the payment is made, and the conditions are satisfied, the authorities issue a compounding order, and the matter is considered settled. The taxpayer is no longer liable for prosecution related to the offence.

No Further Legal Action: After the compounding order is issued, the tax authorities are blocked from initiating any criminal prosecution for the compounded offence.

Compounding Application Fee

“Compounding application fee” refers to a fee that is charged for the process of compounding.

While filing application for compounding of Offence, one should be aware of the initial amounts involved with it.

An Applicant is required to deposit non-refundable Compounding Application Fee as Following:

- ▷ Single Compounding Application- Rs. 25,000 (per application)

- ▷ Consolidated Compounding Application- Rs. 50,000 (per application)

Compounding Charges

(i.e. Amount required to pay for Offences under Compounding)

For the purpose of computation of the compounding charge, the word “tax” means tax including surcharge and any cess.

The charges required to be paid for different offences are specified by the Income Tax Act, some of its examples are as follows:

| SECTION | DESCRIPTION/HEADING OF SECTION | COMPOUNDING CHARGES |

| 276C (1) | Willful Attempt to evade tax | 125% of tax amount evaded |

| 276C (2) | Willful Attempt to evade payment of tax | 1.5% per month or part of month of tax, the payment of which was evaded. |

| 276B/276BB | Failure to pay TDS/TCS | 1.5% per month or part of month of tax in default |

| 276CC | Failure to furnish return | 15% of the amount of tax evaded or Rs 5,00,000, whichever is higher. |

| 277A | Falsification of books of accounts/documents | 100% of amount of tax evaded. |

| 276D | Failure to produce accounts and documents | 10% of assessed or returned income or Rs. 5,00,000 whichever is higher. |

Why Compounding Could Be the Right Choice for You

Advantages of Compounding:

- 1. Faster Resolution: Compounding avoids lengthy court battles, saving your time and legal expenses.

- 2. Reduction in Penalties: The penalties levied in a compounding agreement are often much lower than the potential fines and interest that could accrue if the case were to go to court.

- 3. Avoids Criminal Records: Compounding keeps your record clean, which is especially important for businesses and professionals.

Handling Critical Compounding Offences Cases: AKSSAI’s Expertise in Action

Navigating the complexities of income tax regulations often leads to unintended delays or missed deadlines, which can result in severe penalties. However, businesses may not realize that there are opportunities for redress even in such challenging circumstances. At AKSSAI, we specialize in helping clients who have faced complications due to missed deadlines or mismanagement by previous consultants, offering a path to resolution.

How AKSSAI Stands Out?

At AKSSAI, our focus goes beyond routine tax filings. We are dedicated to exploring every possible legal avenue to protect our client’s interests. Our in-depth knowledge of the Income Tax Act, combined with our strategic approach, allows us to resolve even the most complex cases.

Cases Across India of Compounding of Offences Under the Income Tax

As per the RTI information we received, following cases were filed in different states in the past 10 years:

| States | Cases |

|---|---|

| Gujarat | 942 |

| Karnataka | 690 |

| Meghalaya | 73 |

| Uttar Pradesh | 91 |

| Maharashtra | 138 |

| Tamil Nadu | 125 |

| West Bengal | 6 |

| Madhya Pradesh | 337 |

| Rajasthan | 75 |

| Delhi | 255 |

| Punjab | 125 |

| Andhra Pradesh | 32 |

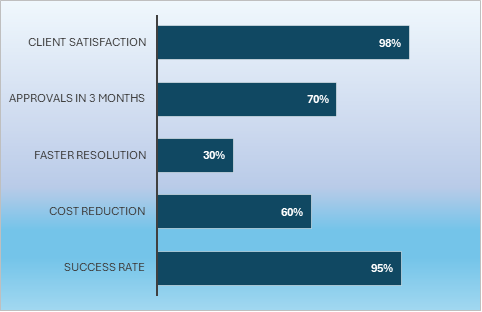

AKSSAI’s Proven Success:

- • 95% Success Rate: Successfully resolved a wide range of compounding cases across multiple industries.

- • Up to 60% Cost Reduction: Minimized legal costs and penalties through effective negotiation.

- • 30% Faster Resolution: Achieved quicker case closures, saving valuable time for clients.

- • 70% Approval in 3 Months: Most clients obtain compounding approval within three months.

- • 98% Client Satisfaction: High retention and referral rates, demonstrating trust and effectiveness.

FAQs after the New Guidelines Dated: 17-10-2024 on Compounding of Offences:

Any taxpayer, company, or person deemed guilty of an offence under the Income Tax Act can apply for compounding, provided he meets the necessary conditions prescribed under the guidelines.

The compounding application can be filed Suo-moto at any time after the offences occur, regardless of whether it has come to the Department’s notice.

Yes, as per Section 279(2) of the Income Tax Act, 1961 provides that any offence under Chapter XXII of the act may be compounded either before or after the institution of proceedings.

Yes, Applications can be filed again under new guidelines issued, if only these applications were rejected under earlier guidelines due to curable defects such as non-payment of Interest, tax, penalty, filing of application in incorrect proforma etc.

Yes, compounding of offences is available for both individuals and companies, provided they have committed offences under the Income Tax Act that are eligible for compounding.

CONCLUSION

Receiving a notice from the tax authorities about an error in your tax filings. You’re worried about penalties and uncertain about the next steps, but there’s a way to handle this without court proceedings — it’s called “Compounding of Offences.” Compounding allows you to settle tax disputes by paying a fee, avoiding court trials and resolving issues more quickly.

The compounding of offences offers a practical solution for taxpayers to resolve tax disputes swiftly and efficiently without the stress of court proceedings. It helps avoid lengthy legal battles, hefty fines, and potential damage to one’s reputation.

Please note the following:

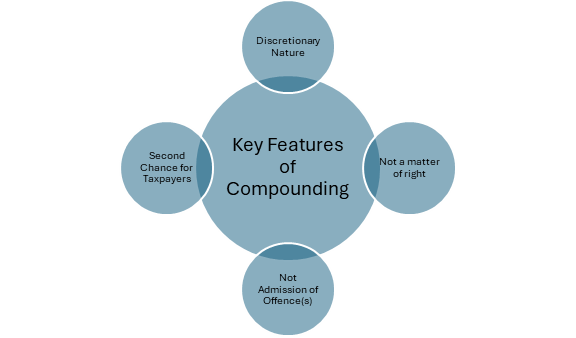

- Compounding is not a Matter of right, it is at the discretion of Competent Authority and applications may be rejected if not filed properly.

- Compounding of Offence is not Admission of Offence(s), instead it is intended to resolve the offence.

- Application for Compounding of Offence can be made anytime, as no time limit is prescribed for it.

- If the Application for Compounding is made beyond 12 months from the end of month in which prosecution complaint is filed, the compounding charges shall be increased by 50% of the amount.

Hence, by keeping the following points in mind, you can make informed decisions that save both time and money. If you find yourself facing a tax-related offence, consider compounding as a proactive approach to safeguard your financial standing and peace of mind.

In a world where the only constant is change, professional help is not just an option, it’s a strategic necessity. In the face of constant legal changes, investing in expert help is an investment in your long-term success.

Our expert team is here to guide you through the process, ensuring a seamless and less intimidating experience.